Archive for the ‘Predictive Analytics’ Category

A gentle introduction to decision trees using R

Introduction

Most techniques of predictive analytics have their origins in probability or statistical theory (see my post on Naïve Bayes, for example). In this post I’ll look at one that has more a commonplace origin: the way in which humans make decisions. When making decisions, we typically identify the options available and then evaluate them based on criteria that are important to us. The intuitive appeal of such a procedure is in no small measure due to the fact that it can be easily explained through a visual. Consider the following graphic, for example:

Figure 1: Example of a simple decision tree (Courtesy: Duncan Hull)

(Original image: https://www.flickr.com/photos/dullhunk/7214525854, Credit: Duncan Hull)

The tree structure depicted here provides a neat, easy-to-follow description of the issue under consideration and its resolution. The decision procedure is based on asking a series of questions, each of which serve to further reduce the domain of possibilities. The predictive technique I discuss in this post,classification and regression trees (CART), works in much the same fashion. It was invented by Leo Breiman and his colleagues in the 1970s.

In what follows, I will use the open source software, R. If you are new to R, you may want to follow this link for more on the basics of setting up and installing it. Note that the R implementation of the CART algorithm is called RPART (Recursive Partitioning And Regression Trees). This is essentially because Breiman and Co. trademarked the term CART. As some others have pointed out, it is somewhat ironical that the algorithm is now commonly referred to as RPART rather than by the term coined by its inventors.

A bit about the algorithm

The rpart algorithm works by splitting the dataset recursively, which means that the subsets that arise from a split are further split until a predetermined termination criterion is reached. At each step, the split is made based on the independent variable that results in the largest possible reduction in heterogeneity of the dependent (predicted) variable.

Splitting rules can be constructed in many different ways, all of which are based on the notion of impurity- a measure of the degree of heterogeneity of the leaf nodes. Put another way, a leaf node that contains a single class is homogeneous and has impurity=0. There are three popular impurity quantification methods: Entropy (aka information gain), Gini Index and Classification Error. Check out this article for a simple explanation of the three methods.

The rpart algorithm offers the entropy and Gini index methods as choices. There is a fair amount of fact and opinion on the Web about which method is better. Here are some of the better articles I’ve come across:

https://www.garysieling.com/blog/sklearn-gini-vs-entropy-criteria

http://www.salford-systems.com/resources/whitepapers/114-do-splitting-rules-really-matter

The answer as to which method is the best is: it depends. Given this, it may be prudent to try out a couple of methods and pick the one that works best for your problem.

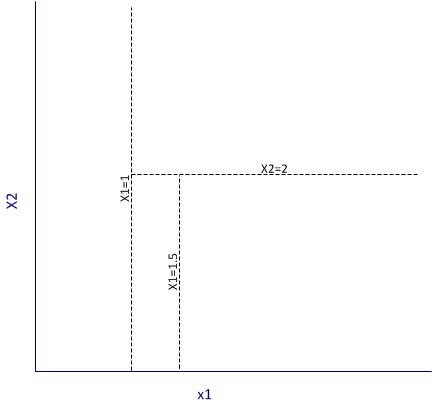

Regardless of the method chosen, the splitting rules partition the decision space (a fancy word for the entire dataset) into rectangular regions each of which correspond to a split. Consider the following simple example with two predictors x1 and x2. The first split is at x1=1 (which splits the decision space into two regions x11), the second at x2=2, which splits the (x1>1) region into 2 sub-regions, and finally x1=1.5 which splits the (x1>1,x2>2) sub-region further.

Figure 2: Example of partitioning

It is important to note that the algorithm works by making the best possible choice at each particular stage, without any consideration of whether those choices remain optimal in future stages. That is, the algorithm makes a locally optimal decision at each stage. It is thus quite possible that such a choice at one stage turns out to be sub-optimal in the overall scheme of things. In other words, the algorithm does not find a globally optimal tree.

Another important point relates to well-known bias-variance tradeoff in machine learning, which in simple terms is a tradeoff between the degree to which a model fits the training data and its predictive accuracy. This refers to the general rule that beyond a point, it is counterproductive to improve the fit of a model to the training data as this increases the likelihood of overfitting. It is easy to see that deep trees are more likely to overfit the data than shallow ones. One obvious way to control such overfitting is to construct shallower trees by stopping the algorithm at an appropriate point based on whether a split significantly improves the fit. Another is to grow a tree unrestricted and then prune it back using an appropriate criterion. The rpart algorithm takes the latter approach.

Here is how it works in brief:

Essentially one minimises the cost,

First, we note that when

An implication of their tendency to overfit data is that decision trees tend to be sensitive to relatively minor changes in the training datasets. Indeed, small differences can lead to radically different looking trees. Pruning addresses this to an extent, but does not resolve it completely. A better resolution is offered by the so-called ensemble methods that average over many differently constructed trees. I’ll discuss one such method at length in a future post.

Finally, I should also mention that decision trees can be used for both classification and regression problems (i.e. those in which the predicted variable is discrete and continuous respectively). I’ll demonstrate both types of problems in the next two sections.

Classification trees using rpart

To demonstrate classification trees, we’ll use the Ionosphere dataset available in the mlbench package in R. I have chosen this dataset because it nicely illustrates the points I wish to make in this post. In general, you will almost always find that algorithms that work fine on classroom datasets do not work so well in the real world…but of course, you know that already!

We begin by setting the working directory, loading the required packages (rpart and mlbench) and then loading the Ionosphere dataset.

Next we separate the data into training and test sets. We’ll use the former to build the model and the latter to test it. To do this, I use a simple scheme wherein I randomly select 80% of the data for the training set and assign the remainder to the test data set. This is easily done in a single R statement that invokes the uniform distribution (runif) and the vectorised function, ifelse. Before invoking runif, I set a seed integer to my favourite integer in order to ensure reproducibility of results.

In the above, I have also removed the training flag from the training and test datasets.

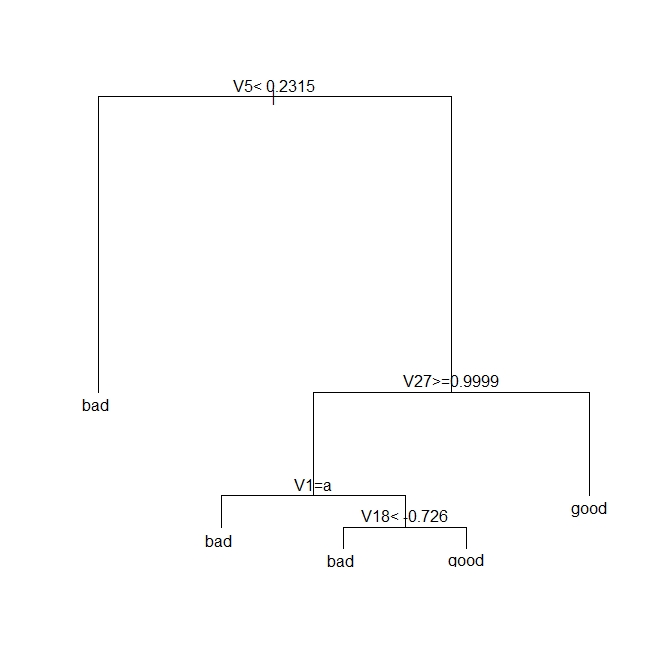

Next we invoke rpart. I strongly recommend you take some time to go through the documentation and understand the parameters and their defaults values. Note that we need to remove the predicted variable from the dataset before passing the latter on to the algorithm, which is why we need to find the column index of the predicted variable (first line below). Also note that we set the method parameter to “class“, which simply tells the algorithm that the predicted variable is discrete. Finally, rpart uses Gini rule for splitting by default, and we’ll stick with this option.

The resulting plot is shown in Figure 3 below. It is quite self-explanatory so I won’t dwell on it here.

Figure 3: A classification tree for Ionosphere dataset

Next we see how good the model is by seeing how it fares against the test data.

| pred true | bad | good |

| bad | 17 | 2 |

| good | 9 | 43 |

Note that we need to verify the above results by doing multiple runs, each using different training and test sets. I will do this later, after discussing pruning.

Next, we prune the tree using the cost complexity criterion. Basically, the intent is to see if a shallower subtree can give us comparable results. If so, we’d be better of choosing the shallower tree because it reduces the likelihood of overfitting.

As described earlier, we choose the appropriate pruning parameter (aka cost-complexity parameter)

| CP | nsplit | rel error | xerror | xstd | |

| 1 | 0.57 | 0 | 1.00 | 1.00 | 0.080178 |

| 2 | 0.20 | 1 | 0.43 | 0.46 | 0.062002 |

| 3 | 0.02 | 2 | 0.23 | 0.26 | 0.048565 |

| 4 | 0.01 | 4 | 0.19 | 0.35 |

It is clear from the above, that the lowest cross-validation error (xerror in the table) occurs for

Next, we prune the tree based on this value of CP:

Note that rpart will use a default CP value of 0.01 if you don’t specify one in prune.

The pruned tree is shown in Figure 4 below.

Figure 4: A pruned classification tree for Ionosphere dataset

Let’s see how this tree stacks up against the fully grown one shown in Fig 3.

This seems like an improvement over the unpruned tree, but one swallow does not a summer make. We need to check that this holds up for different training and test sets. This is easily done by creating multiple random partitions of the dataset and checking the efficacy of pruning for each. To do this efficiently, I’ll create a function that takes the training fraction, number of runs (partitions) and the name of the dataset as inputs and outputs the proportion of correct predictions for each run. It also optionally prunes the tree. Here’s the code:

Note that in the above, I have set the default value of the prune_tree to FALSE, so the function will execute the first branch of the if statement unless the default is overridden.

OK, so let’s do 50 runs with and without pruning, and check the mean and variance of the results for both sets of runs.

So we see that there is an improvement of about 3% with pruning. Also, if you were to plot the trees as we did earlier, you would see that this improvement is achieved with shallower trees. Again, I point out that this is not always the case. In fact, it often happens that pruning results in worse predictions, albeit with better reliability – a classic illustration of the bias-variance tradeoff.

Regression trees using rpart

In the previous section we saw how one can build decision trees for situations in which the predicted variable is discrete. Let’s now look at the case in which the predicted variable is continuous. We’ll use the Boston Housing dataset from the mlbench package. Much of the discussion of the earlier section applies here, so I’ll just display the code, explaining only the differences.

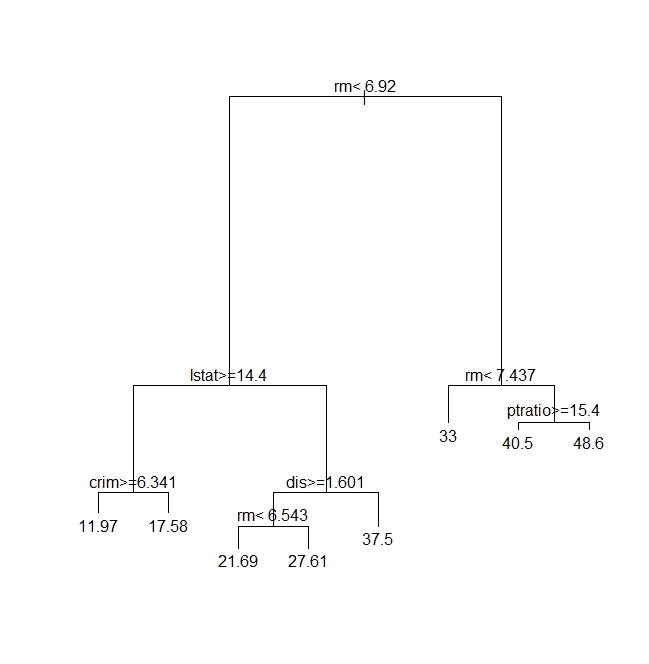

Next we invoke rpart, noting that the predicted variable is medv (median value of owner-occupied homes in $1000 units) and that we need to set the method parameter to “anova“. The latter tells rpart that the predicted variable is continuous (i.e that this is a regression problem).

The plot of the tree is shown in Figure 5 below.

Figure 5: A regression tree for Boston Housing dataset

Next, we need to see how good the predictions are. Since the dependent variable is continuous, we cannot compare the predictions directly against the test set. Instead, we calculate the root mean square (RMS) error. To do this, we request rpart to output the predictions as a vector – one prediction per record in the test dataset. The RMS error can then easily be calculated by comparing this vector with the medv column in the test dataset.

Here is the relevant code:

Again, we need to do multiple runs to check on the reliability of the predictions. However, you already know how to do that so I will leave it to you.

Moving on, we prune the tree using the cost complexity criterion as before. The code is exactly the same as in the classification problem.

The tree is unchanged so I won’t show it here. This means, as far as the cost complexity pruning is concerned, the optimal subtree is the same as the original tree. To confirm this, we’d need to do multiple runs as before – something that I’ve already left as as an exercise for you :). Basically, you’ll need to write a function analogous to the one above, that computes the root mean square error instead of the proportion of correct predictions.

Wrapping up

This brings us to the end of my introduction to classification and regression trees using R. Unlike some articles on the topic I have attempted to describe each of the steps in detail and provide at least some kind of a rationale for them. I hope you’ve found the description and code snippets useful.

I’ll end by reiterating a couple points I made early in this piece. The nice thing about decision trees is that they are easy to explain to the users of our predictions. This is primarily because they reflect the way we think about how decisions are made in real life – via a set of binary choices based on appropriate criteria. That said, in many practical situations decision trees turn out to be unstable: small changes in the dataset can lead to wildly different trees. It turns out that this limitation can be addressed by building a variety of trees using different starting points and then averaging over them. This is the domain of the so-called random forest algorithm.We’ll make the journey from decision trees to random forests in a future post.

Postscript, 20th September 2016: I finally got around to finishing my article on random forests.

A gentle introduction to Naïve Bayes classification using R

Preamble

One of the key problems of predictive analytics is to classify entities or events based on a knowledge of their attributes. An example: one might want to classify customers into two categories, say, ‘High Value’ or ‘Low Value,’ based on a knowledge of their buying patterns. Another example: to figure out the party allegiances of representatives based on their voting records. And yet another: to predict the species a particular plant or animal specimen based on a list of its characteristics. Incidentally, if you haven’t been there already, it is worth having a look at Kaggle to get an idea of some of the real world classification problems that people tackle using techniques of predictive analytics.

Given the importance of classification-related problems, it is no surprise that analytics tools offer a range of options. My favourite (free!) tool, R, is no exception: it has a plethora of state of the art packages designed to handle a wide range of problems. One of the problems with this diversity of choice is that it is often confusing for beginners to figure out which one to use in a particular situation. Over the next several months, I intend to write up tutorial articles covering many of the common algorithms, with a particular focus on their strengths and weaknesses; explaining where they work well and where they don’t. I’ll kick-off this undertaking with a simple yet surprisingly effective algorithm – the Naïve Bayes classifier.

Just enough theory

I’m going to assume you have R and RStudio installed on your computer. If you need help with this, please follow the instructions here.

To introduce the Naive Bayes algorithm, I will use the HouseVotes84 dataset, which contains US congressional voting records for 1984. The data set is in the mlbench package which is not part of the base R installation. You will therefore need to install it if you don’t have it already. Package installation is a breeze in RStudio – just go to Tools > Install Packages and follow the prompts.

The HouseVotes84 dataset describes how 435 representatives voted – yes (y), no (n) or unknown (NA) – on 16 key issues presented to Congress. The dataset also provides the party affiliation of each representative – democrat or republican.

Let’s begin by exploring the dataset. To do this, we load mlbench, fetch the dataset and get some summary stats on it. (Note: a complete listing of the code in this article can be found here)

It is good to begin by exploring the data visually. To this end, let’s do some bar plots using the basic graphic capabilities of R:

The plots are shown in Figures 1 through 3.

Fig 1: y and n votes for issue 1

Fig 2: Republican votes for issue 1.

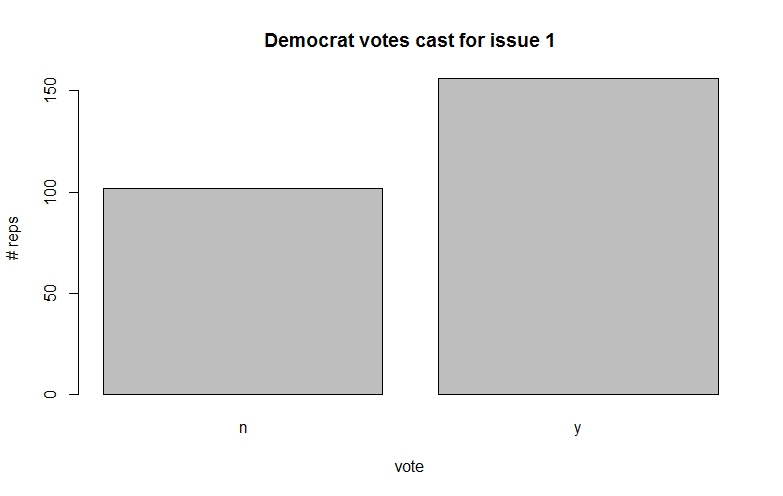

Fig 3: Democrat votes for issue 1.

Among other things, such plots give us a feel for the probabilities associated with how representatives from parties tend to vote on specific issues.

The classification problem at hand is to figure out the party affiliation from a knowledge of voting patterns. For simplicity let us assume that there are only 3 issues voted on instead of the 16 in the actual dataset. In concrete terms we wish to answer the question, “what is the probability that a representative is, say, a democrat (D) given that he or she has voted, say,

In the notation of conditional probability this can be written as,

(Note: If you need a refresher on conditional probability, check out this post for a simple explanation.)

By Bayes theorem, which I’ve explained at length in this post, this can be recast as,

We’re interested only in relative probabilities of the representative being a democrat or republican because the predicted party affiliation depends only on which of the two probabilities is larger (the actual value of the probability is not important). This being the case, we can factor out any terms that are constant. As it happens, the denominator of the above equation – the probability of a particular voting pattern – is a constant because it depends on the total number of representatives (from both parties) who voted a particular way.

Now, using the chain rule of conditional probability, we can rewrite the numerator as:

Basically, the second term on the left hand side,

Another application of the chain rule gives:

Where we have now factored out the n vote on the second issue.

The key assumption of Naïve Bayes is that the conditional probability of each feature given the class is independent of all other features. In mathematical terms this means that,

and

The quantity of interest, the numerator of equation (1) can then be written as:

The assumption of independent conditional probabilities is a drastic one. What it is saying is that the features are completely independent of each other. This is clearly not the case in the situation above: how representatives vote on a particular issue is coloured by their beliefs and values. For example, the conditional probability of voting patterns on socially progressive issues are definitely not independent of each other. However, as we shall see in the next section, the Naïve Bayes assumption works well for this problem as it does in many other situations where we know upfront that it is grossly incorrect.

Another good example of the unreasonable efficacy of Naive Bayes is in spam filtering. In the case of spam, the features are individual words in an email. It is clear that certain word combinations tend to show up consistently in spam – for example, “online”, “meds”, “Viagra” and “pharmacy.” In other words, we know upfront that their occurrences are definitely not independent of each other. Nevertheless, Naïve Bayes based spam detectors which assume mutual independence of features do remarkably well in distinguishing spam from ham.

Why is this so?

To explain why, I return to a point I mentioned earlier: to figure out the affiliation associated with a particular voting pattern (say, v1=y, v2=n,v3=y) one only needs to know which of the two probabilities

This hints as to why the independence assumption might not be so quite so idiotic. Since the prediction depends only the on the maximum, the algorithm will get it right even if there are dependencies between feature providing the dependencies do not change which class has the maximum probability (once again, note that only the maximal class is important here, not the value of the maximum).

Yet another reason for the surprising success of Naïve Bayes is that dependencies often cancel out across a large set of features. But, of course, there is no guarantee that this will always happen.

In general, Naïve Bayes algorithms work better for problems in which the dependent (predicted) variable is discrete, even when there are dependencies between features (spam detection is a good example). They work less well for regression problems – i.e those in which predicted variables are continuous.

I hope the above has given you an intuitive feel for how Naïve Bayes algorithms work. I don’t know about you, but my head’s definitely spinning after writing out all that mathematical notation.

It’s time to clear our heads by doing some computation.

Naïve Bayes in action

There are a couple of well-known implementations of Naïve Bayes in R. One of them is the naiveBayes method in the e1071 package and the other is NaiveBayes method in the klaR package. I’ll use the former for no other reason than it seems to be more popular. That said, I have used the latter too and can confirm that it works just as well.

We’ve already loaded and explored the HouseVotes84 dataset. One of the things you may have noticed when summarising the data is that there are a fair number of NA values. Naïve Bayes algorithms typically handle NA values either by ignoring records that contain any NA values or by ignoring just the NA values. These choices are indicated by the value of the variable na.action in the naiveBayes algorithm, which is set to na.omit (to ignore the record) or na.pass (to ignore the value).

Just for fun, we’ll take a different approach. We’ll impute NA values for a given issue and party by looking at how other representatives from the same party voted on the issue. This is very much in keeping with the Bayesian spirit: we infer unknowns based on a justifiable belief – that is, belief based on the evidence.

To do this I write two functions: one to compute the number of NA values for a given issue (vote) and class (party affiliation), and the other to calculate the fraction of yes votes for a given issue (column) and class (party affiliation).

sum_y<-sum(HouseVotes84[,col]==’y’ & HouseVotes84$Class==cls,na.rm = TRUE)

sum_n<-sum(HouseVotes84[,col]==’n’ & HouseVotes84$Class==cls,na.rm = TRUE)

return(sum_y/(sum_y+sum_n))}

Before proceeding, you might want to go back to the data and convince yourself that these values are sensible.

We can now impute the NA values based on the above. We do this by randomly assigning values ( y or n) to NAs, based on the proportion of members of a party who have voted y or n. In practice, we do this by invoking the uniform distribution and setting an NA value to y if the random number returned is less than the probability of a yes vote and to n otherwise. This is not as complicated as it sounds; you should be able to figure the logic out from the code below.

if(sum(is.na(HouseVotes84[,i])>0)) {

c1 <- which(is.na(HouseVotes84[,i])& HouseVotes84$Class==’democrat’,arr.ind = TRUE)

c2 <- which(is.na(HouseVotes84[,i])& HouseVotes84$Class==’republican’,arr.ind = TRUE)

HouseVotes84[c1,i] <-

ifelse(runif(na_by_col_class(i,’democrat’))<p_y_col_class(i,’democrat’),’y’,’n’)

HouseVotes84[c2,i] <-

ifelse(runif(na_by_col_class(i,’republican’))<p_y_col_class(i,’republican’),’y’,’n’)}

Note that the which function filters indices by the criteria specified in the arguments and ifelse is a vectorised conditional function which enables us to apply logical criteria to multiple elements of a vector.

At this point it is a good idea to check that the NAs in each column have been set according to the voting patterns of non-NAs for a given party. You can use the p_y_col_class() function to check that the new probabilities are close to the old ones. You might want to do this before you proceed any further.

The next step is to divide the available data into training and test datasets. The former will be used to train the algorithm and produce a predictive model. The effectiveness of the model will then be tested using the test dataset. There is a great deal of science and art behind the creation of training and testing datasets. An important consideration is that both sets must contain records that are representative of the entire dataset. This can be difficult to do, especially when data is scarce and there are predictors that do not vary too much…or vary wildly for that matter. On the other hand, problems can also arise when there are redundant predictors. Indeed, the much of the art of successful prediction lies in figuring out which predictors are likely to lead to better predictions, an area known as feature selection. However, that’s a topic for another time. Our current dataset does not suffer from any of these complications so we’ll simply divide the it in an 80/20 proportion, assigning the larger number of records to the training set.

Now we’re finally good to build our Naive Bayes model (machine learning folks call this model training rather than model building – and I have to admit, it does sound a lot cooler).

The code to train the model is anticlimactically simple:

Here we’ve invokedthe naiveBayes method from the e1071 package. The first argument uses R’s formula notation.In this notation, the dependent variable (to be predicted) appears on the left hand side of the ~ and the independent variables (predictors or features) are on the right hand side. The dot (.) is simply shorthand for “all variable other than the dependent one.” The second argument is the dataframe that contains the training data. Check out the documentation for the other arguments of naiveBayes; it will take me too far afield to cover them here. Incidentally, you can take a look at the model using the summary() or str() functions, or even just entering the model name in the R console:

Note that I’ve suppressed the output above.

Now that we have a model, we can do some predicting. We do this by feeding our test data into our model and comparing the predicted party affiliations with the known ones. The latter is done via the wonderfully named confusion matrix – a table in which true and predicted values for each of the predicted classes are displayed in a matrix format. This again is just a couple of lines of code:

| pred true | democrat | republican |

| democrat | 38 | 3 |

| republican | 5 | 22 |

The numbers you get will be different because your training/test sets are almost certainly different from mine.

In the confusion matrix (as defined above), the true values are in columns and the predicted values in rows. So, the algorithm has correctly classified 38 out of 43 (i.e. 38+5) Democrats and 22 out of 25 Republicans (i.e. 22+3). That’s pretty decent. However, we need to keep in mind that this could well be quirk of the choice of dataset. To address this, we should get a numerical measure of the efficacy of the algorithm and for different training and testing datasets. A simple measure of efficacy would be the fraction of predictions that the algorithm gets right. For the training/testing set above, this is simply 60/68 (see the confusion matrix above). The simplest way to calculate this in R is:

A natural question to ask at this point is: how good is this prediction. This question cannot be answered with only a single run of the model; we need to do many runs and look at the spread of the results. To do this, we’ll create a function which takes the number of times the model should be run and the training fraction as inputs and spits out a vector containing the proportion of correct predictions for each run. Here’s the function

I’ve not commented the above code as it is essentially a repeat of the steps described earlier. Also, note that I have not made any effort to make the code generic or efficient.

Let’s do 20 runs with the same training fraction (0.8) as before:

[9] 0.9102564 0.9080460 0.9139785 0.9200000 0.9090909 0.9239130 0.9605263 0.9333333

[17] 0.9052632 0.8977273 0.9642857 0.8518519

0.8519 0.9074 0.9170 0.9177 0.9310 0.9643

We see that the outcome of the runs are quite close together, in the 0.85 to 0.95 range with a standard deviation of 0.025. This tells us that Naive Bayes does a pretty decent job with this data.

Wrapping up

I originally intended to cover a few more case studies in this post, a couple of which highlight the shortcomings of the Naive Bayes algorithm. However, I realize that doing so would make this post unreasonably long, so I’ll stop here with a few closing remarks, and a promise to write up the rest of the story in a subsequent post.

To sum up: I have illustrated the use of a popular Naive Bayes implementation in R and attempted to convey an intuition for how the algorithm works. As we have seen, the algorithm works quite well in the example case, despite the violation of the assumption of independent conditional probabilities.

The reason for the unreasonable effectiveness of the algorithm is two-fold. Firstly, the algorithm picks the predicted class based on the largest predicted probability, so ordering is more important than the actual value of the probability. Secondly, in many cases, a bias one way for a particular vote may well be counteracted by a bias the other way for another vote. That is, biases tend to cancel out, particularly if there are a large number of features.

That said, there are many cases in which the algorithm fails miserably – and we’ll look at some of these in a future post. However, despite its well known shortcomings, Naive Bayes is often the first port of call in prediction problems simply because it is easy to set up and is fast compared to many of the iterative algorithms we will explore later in this series of articles.

Endnote

Thanks for reading! If you liked this piece, you might enjoy the other articles in my “Gentle introduction to analytics using R” series. Here are the links:

A gentle introduction to text mining using R